|

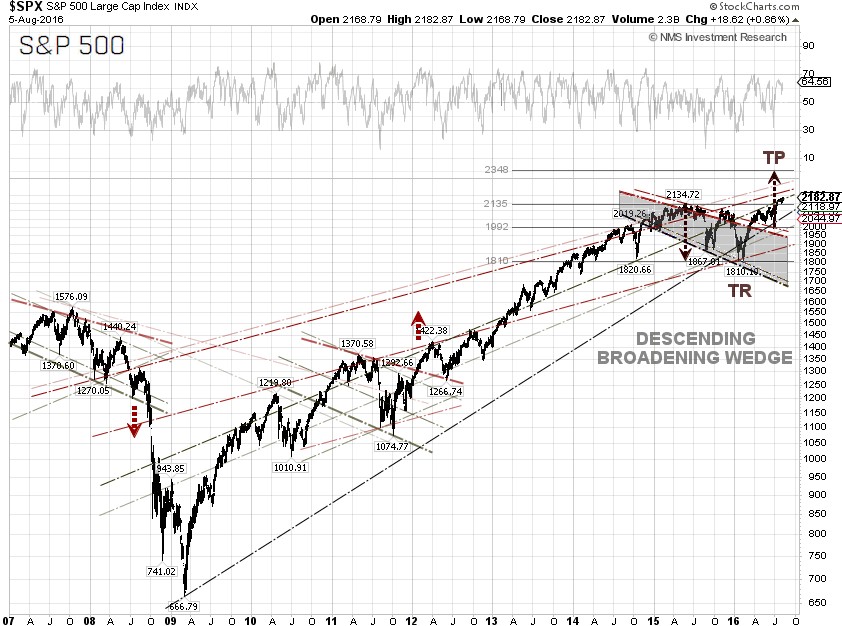

The S&P 500 inched up 0.43% for the week, to close at 2,182.87 on Friday, along with crude oil prices, in tandem with other market moving economic events, including monetary policy decisions on interest rates by central banks. The index surged 0.86% on Friday after the U.S. Labor Department reported that nonfarm payrolls increased by seasonally adjusted 255,000 jobs last month, beating Wall Street economists' forecast of an 180,000 gain. If not seasonally adjusted, the nonfarm payrolls were 1.03 million jobs lost for July, according to Table B-1. The May figures were revised upward from 11,000 to 24,000, and the change for June was revised from 287,000 to 292,000.

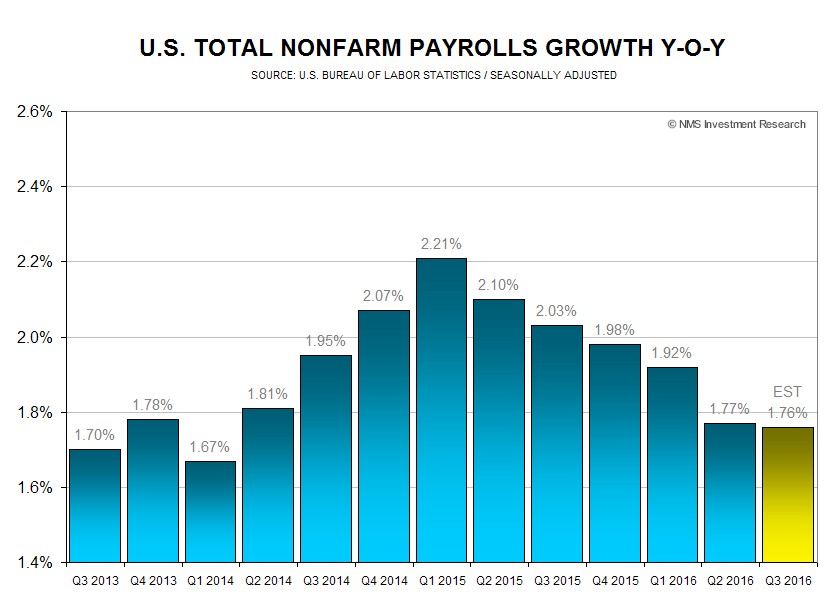

The U.S. unemployment rate held at 4.9% in July, with total nonfarm payrolls standing at 144.448 million. If 200,000 jobs are added for August and September each, total nonfarm payrolls growth will be just 1.76% for the third-quarter 2016, the slowest since the second-quarter 2014. Slow growth could be due to lack of qualified workers, as the labor market approaches maximum employment. Nonetheless, with a labor force participation rate of only 62.8%, some 94.3 million Americans might still be looking for a job.

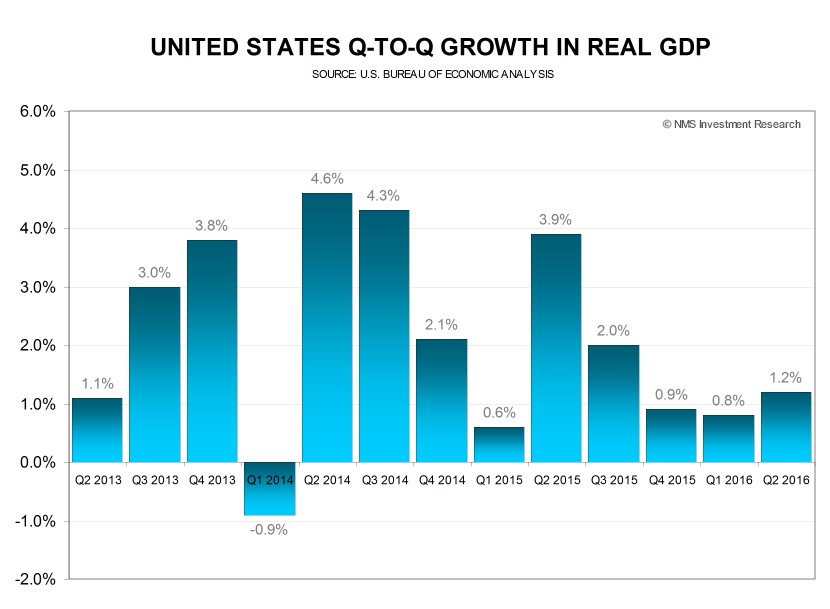

Both U.S. total nonfarm payrolls and economic growth are decelerating. The market got a big surprise after the U.S. Bureau of Economic Analysis released the second-quarter GDP (advance estimate) last Friday, showing a disappointing GDP of 1.2%. So far this year, the U.S. economy is growing at about a 1% annual rate, the worst first-half performance since 2011. GDP growth was revised down to a 0.8% pace in the first-quarter, from 1.1%. Growth also was revised downward for the fourth-quarter of 2015 to 0.9%, from 1.4%. The Federal Reserve bank of New York currently forecasts the third-quarter GDP at 2.6%.

The probability of a 25 basis point rate hike at the next FOMC meeting on September 21 jumped 9 percentage points from 18.0% before the release of the nonfarm payrolls report, while the probability of a no rate hike dropped to 82.0% from 91.0%, according to data from the CME Group as of August 5.

The best performing S&P 500 sectors for the week were Information technology, and Financials, up 1.63%, and 1.41%, respectively. The worst performing sectors for the week were Utilities and Telecommunication Services, down 2.68% and 1.82%, respectively.

|