|

The WTI crude oil spot price continued to skyrocket, to close on Friday at $49.11 per barrel, up 10.38% for the week, while the Brent crude price jumped 7.8% for the week to close at $50.85 per barrel, following a weaker dollar, a bullish EIA oil inventory report and comments from Russia Energy Minister Alexander Novak. Mr. Novak told Saudi-owned newspaper Asharq al-Awsat on Monday that a complete return of market stability is only likely in 2017 and dialogue with Saudi Arabia regarding a possible deal aimed at achieving long-term oil market stability has progressed in "a tangible way", according to a Reuters report.

Iran is still a wild card though, as its officials said in April that Iran wouldn't participate in any negotiations until it restored production to pre-sanction levels, between 4 million and 4.2 million barrels per day (bpd), according to a Bloomberg report. On Tuesday, an Iranian press official told the Wall Street Journal that the country likely would not be pumping that much oil by September, ahead of OPEC’s informal meeting.

The EIA weekly U.S. oil inventory report on Wednesday showed a decline of 2.51 million barrels to 521.1 million barrels, excluding strategic inventories, in the week ending August 12, compared to S&P Global Platts analysts’ expectations for a drawdown of 200,000 barrels. The American Petroleum Institute (API) inventory data on Tuesday showed a U.S. crude inventory drawdown of 1.0 million barrels for the week.

There was a decline last week in U.S. gasoline supplies of 2.7 million barrels, while distillate stockpiles, including jet fuel, diesel fuel and heating oil, increased by 1.9 million barrels, according to the EIA. Analysts were expecting a drawdown of 1.8 million barrels of gasoline stocks and a drop of 500,000 barrels for distillates.

Separately, the EIA said the weekly U.S. crude oil production increased by 152,000 bpd for the week ending August 12, 2016, to 8.597 million bpd. Weekly U.S. crude oil output has fallen about 10.54% from the peak level of 9.61 million bpd during the week ending August 12, 2015. Houston-based oilfield services company Baker Hughes Inc. said on Friday that the U.S. oil rig count was up another 10 from the previous week, to 406, compared to 316, when the rig count hit the low on June 6, 2016.

The best performing S&P 500 sectors for the week were Energy and Materials, up 1.97% and 1.27%, respectively. The worst performing sectors for the week were Telecommunication services and Utilities, down 3.84% and 1.29%, respectively.

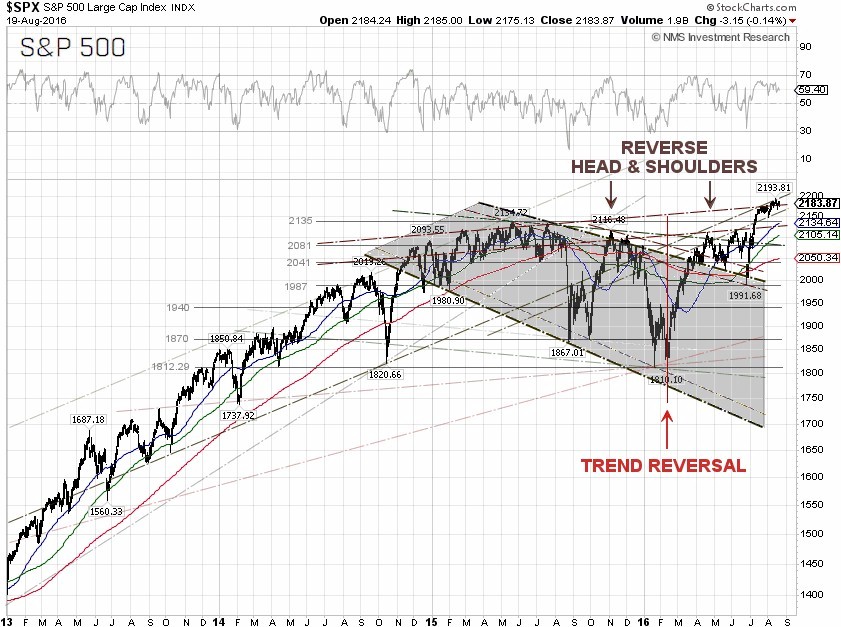

S&P 500 Summary: +6.85% YTD as of 08/19/16

Barclay Hedge Fund Index: +2.68% YTD

Outperforming Sectors: Energy +15.55% YTD, Utilities +15.52% YTD, Telecommunication services +15.26% YTD, Materials +12.09% YTD, Industrials +10.11% YTD, Information technology +8.58% YTD, and Consumer staples +8.38% YTD.

Underperforming Sectors: Consumer discretionary +4.07% YTD, Healthcare +3.0% YTD, and Financials +0.39%

YTD. |