|

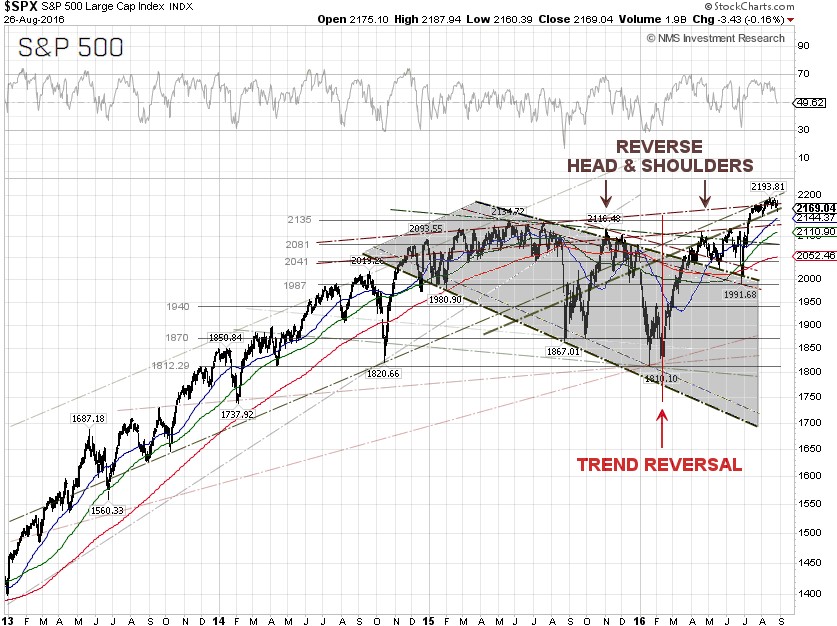

The S&P 500 closed at 2,169.04 on Friday, down 0.68% for the week, as the OPEC rumor mill runs out of steam and crude oil prices begin to sag. At 2:02 p.m. EST on Wednesday, August 24, 2016, Hillary Clinton tweeted the following: Hillary Clinton

(@HillaryClinton) - EpiPens can be the difference between life and death. There's no justification for these price hikes.

https://t.co/O6RbVR6Qim -H. The S&P 500 Healthcare sector tumbled 1.51% and wiped out about $45 billion of its market capitalization after Clinton’s tweet hit the Bloomberg terminal. For the week, the S&P 500 Healthcare sector, one of the worst performers this year, lost 1.80%.

The speech by Federal Reserve Chair Janet Yellen at the Kansas City Fed’s annual economic symposium in Jackson Hole, Wyoming on Friday was a non-event. After running up 0.71% to an intraday high of 2,187.94, the S&P 500, however, took a U-turn following comments from Stanley Fischer, Vice Chairman of the U.S. Federal Reserve, in an interview with CNBC shortly after Yellen’s speech. Fischer told a CNBC reporter that the central bank could possibly raise interest rates twice before the end of 2016, depending on the strength of economic data released in the coming months.

Many Fed observers believe that Fischer’s comments overshadowed the earlier remarks from

Yellen, who said, “In light of the continued solid performance of the labor market and our outlook for economic activity and inflation, I believe the case for an increase in the federal funds rate has strengthened in recent months.”. The FX market interpreted Yellen’s remarks as the odds of an interest rate hike were roughly even for the Fed's December policy meeting.

The U.S. Dollar index jumped 1.12% for the week, to close on Friday at 95.542, mostly on Friday after Fischer’s comments, while the yield of the 10-year U.S. Treasury Note surged 2.53% to close at 1.62% on Friday. The yield spread between the 10-year and 2-year U.S. Treasury Notes narrowed to 0.78 percentage points at the close on Friday, as recession fears rose.

The probability of a 25 basis point rate hike at the next FOMC meeting on September 21 jumped to 36.0%, while the probability of a no change in monetary policy stands at 64.0%, based on the CME Group 30-day Fed Fund futures prices as of August 26. From the Fed’s “Dot-Plot”, or the FOMC’s participant survey, the Fed Funds target rate is between 0.75 and 1.0%, meaning two more rate hikes are possibly on the table this year.

|