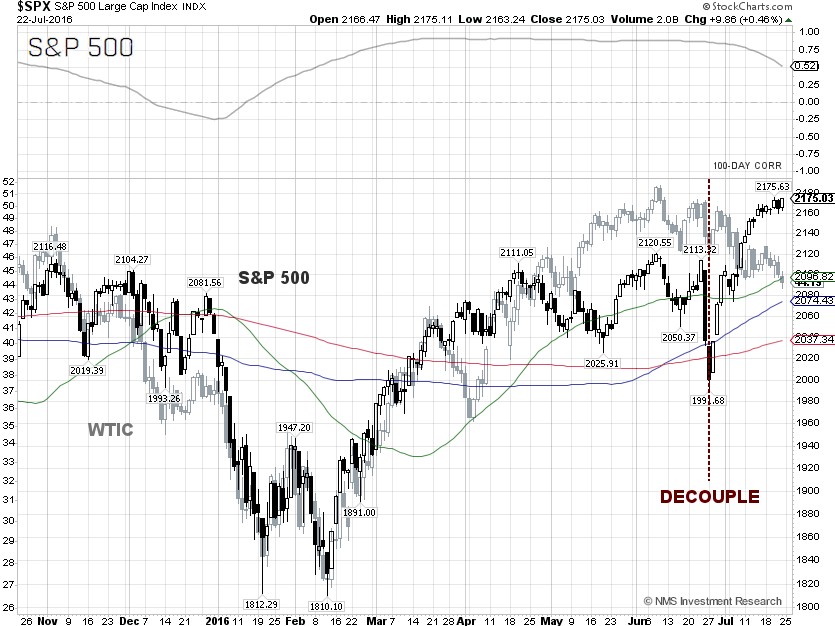

|

There was another large build last week in U.S. gasoline supplies of 900,000 barrels, while distillate stockpiles, including jet fuel, diesel fuel and heating oil, dropped 200,000 barrels, according to the EIA. Analysts were expecting the gasoline stocks to remain unchanged and a rise of 700,000 barrels for distillates.

Separately, the EIA said the weekly U.S. crude oil production decreased by 9,000 barrels per day (bpd) for the week ending July 15, 2016, to 8.494 million bpd. Weekly U.S. crude oil output has fallen about 11.61% from the peak level of 9.61 million bpd during the week ending June 6, 2015. Houston-based oilfield services company Baker Hughes Inc. said on Friday that the U.S. oil rig count was up another 14 from the previous week, to 371, compared to 316, when the rig count hit the low on June 6.

There are still no discussions between OPEC and Russia about oil output after a failed attempt to jointly maintain production levels earlier this year. OPEC’s monthly report stated that Saudi Arabia’s crude oil production rose by 66,500 bpd, to 10.3 million bpd in June 2016, compared to the previous month, while Iran’s crude oil production rose by 77,800 bpd, to 3.64 million bpd in June 2016, compared to May 2016. Iran almost doubled its exports since early 2016. Russia’s crude oil production also rose to 10.8 million bpd in June 2016, compared to the previous month, according to the Russian Energy Ministry.

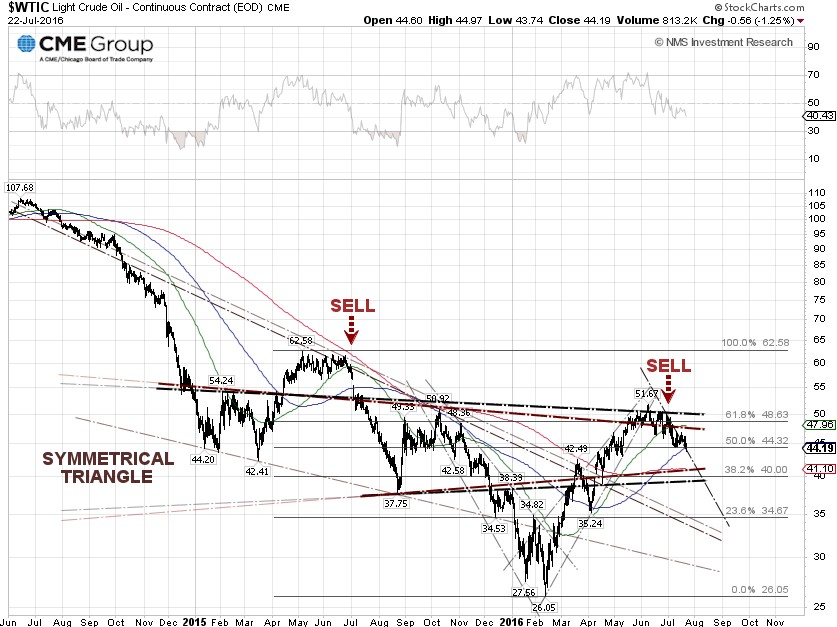

Technically, the WTI crude price broke down the $44.32 support, or the 50.0% Fibonacci retracement level, as demand remains soft. The next support is the $40.00 per barrel level, or 38.2% Fibonacci retracement. The EIA cut U.S. oil demand on July 12 to 160,000 bpd in 2016, compared with previous expectations for 220,000 bpd. If the $40.00 level can’t hold, the next support is $34.67, or the 23.6% Fibonacci retracement level.

U.S. economic data released this week were mixed. The global financial information and services firm Markit, said on Friday that its July U.S. Manufacturing Flash Purchasing Managers' (PMI) Index rose to 52.9 from 51.3 in June. A PMI reading above 50 indicates expansion in the sector. This reading was better than the analyst consensus estimate of 51.6, according to a Thomson Reuters poll.

The U.S. Manufacturing PMI has been in a downtrend since it peaked at 57.3 in June 2014 and bottomed at 50.5 in May 2016. Markit chief economist, Chris Williamson said, “It remains too early to say if this is the start of a stronger upturn, but this is a welcome and encouraging sign of revival after the second quarter, in which the PMI signaled the sector’s worst performance for over six years.”

Also released on Friday was the July Philadelphia Federal Reserve’s index of business conditions, or Philly Fed, which came in at negative 2.9%, compared to the positive 3.5 expected by economists polled by MarketWatch. This is the ninth month of declining activity in the past eleven months, and the slowest pace in six months.

Last Friday, the Federal Reserve said U.S. industrial production rose a seasonally adjusted 0.6% in June, beating the 0.4% forecasted rise from economists surveyed by The Wall Street Journal. Separately, the Federal Reserve Bank of New York also said last Friday that its Empire State manufacturing index tumbled to a reading of 0.55 in July, missing the forecast of 5.0. Any reading above zero points to expansion. |