|

The WTI crude spot price surged 3.24%, closing at $52.24 per barrel on Friday, while the Brent crude spot price was up 2.93% to close at $55.19 per barrel, despite another bearish EIA weekly report. It sounds like Goldman Sachs is backstopping WTI crude prices, when the firm sent out a research note on Wednesday saying that with global demand exceeding supply, they are "constructive" on oil prices, at least in the short term. Goldman said, "We project WTI will increase from $50/bbl to $57.50/bbl by mid-year and average of $55/bbl in “the second half of 2017", according to Barrons.

Just about two weeks ago, on March 21, Goldman Sachs sent out a research note saying that 2017-19 is likely to see the largest increase in history for mega projects' production, as the record 2011-13 capex commitment yields fruit, meaning a possible record for non-OPEC production growth in 2018. The WTI crude spot price tumbled 1.37% that day to $48.24 per barrel, below the 200-day SMA. Crude oil prices were also given a boost after the U.S. launched cruise missiles at a Syrian base on Thursday, in response to a chemical weapons attack in Syria that killed more than 100 civilians earlier in the week.

The EIA weekly U.S. oil inventory report on Wednesday showed that domestic crude supplies increased by 1.57 million barrels to an all-time high of 535.54 million barrels, excluding the Strategic Petroleum Reserve, in the week ending March 31, compared to the Wall Street Journal forecast for a stockpile decline of 0.2 million barrels. The American Petroleum Institute, or API, inventory data on Tuesday showed a U.S. crude inventory decline of 1.8 million barrels.

Separately, the EIA said the weekly U.S. crude oil production increased 52,000 barrels per day, or bpd, for the week ending March 31, to 9.199 million bpd. U.S. crude oil output increased 137,000 bpd to an average of 9.134 million bpd in March, compared to a February average of 8.997 million bpd. Output has fallen just 4.85% from the peak level of 9.60 million bpd in June 2015. Houston-based oilfield services company Baker Hughes Inc. said on Friday that the U.S. oil rig count rose another 10 to 672, compared to 316, when the rig count hit the low on June 6, 2016.

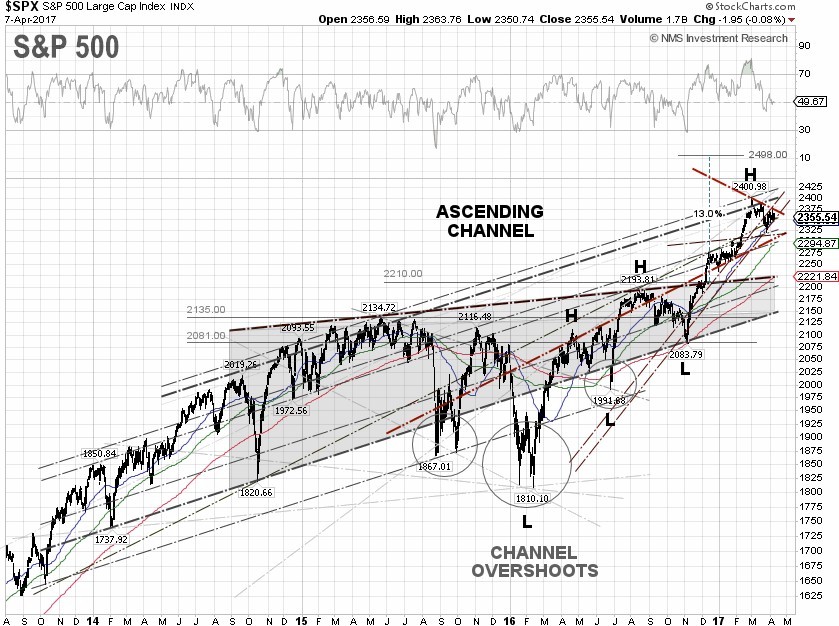

S&P 500 Summary: +5.21% YTD as of 04/07/17

Barclay Hedge Fund Index: +2.75% YTD

Outperforming Sectors: Information technology +11.51 YTD, Healthcare +7.90% YTD, Consumer discretionary +7.21% YTD, Consumer staples +5.77% YTD, Materials +5.63% YTD, and Utilities +5.62% YTD.

Underperforming Sectors: Industrials +4.08% YTD, Real Estate +3.37% YTD, Financials +1.08% YTD, Telecommunication services –6.10% YTD, and Energy –6.74%

YTD. |