|

The yield of 10-year U.S. Treasury Notes ticked down 0.46% this week, to close on Friday at 2.389%, while the yield spread between the 10-year and 2-year U.S. Treasury Notes narrowed to 1.13 percentage points. The spot gold price was up another 0.22% for the week, to close at $1,251.20 per ounce on Friday, while the Japanese yen is flat against the U.S. dollar.

The WTI crude spot price surged 5.27% for the week, closing at $50.50 per barrel on Friday, while the Brent crude spot price jumped 4.89% for the week to close at $53.62 per barrel, despite a bearish EIA weekly report showing the crude oil inventory stood at another record level and U.S. production continued to rise. Traders ran up crude prices anyway after the EIA said that gasoline supplies dropped 3.7 million barrels, while distillate stockpiles fell 2.5 million barrels last week, compared to the S&P Global Platts survey forecast for a fall of 2.1 million barrels of gasoline and decline of 1.1 million barrels for distillates.

Bloomberg reported, from unnamed sources in Libya on Wednesday, that Libya’s largest oil field, Sharara, mysteriously stopped producing. Separately, according to Reuters, a joint committee of ministers from OPEC and non-OPEC oil producers agreed to review whether a global pact to limit supplies should be extended by six months. Although the Bloomberg report was unsubstantiated, and the six-month extension of the output cut by OPEC and non-OPEC was just talk, traders were quick to cover their short positions, according to data from the U.S. Commodity Futures Trading Commission, or CFTC.

The EIA weekly U.S. oil inventory report on Wednesday showed that domestic crude supplies increased by 0.867 million barrels to an all-time high of 533.98 million barrels, excluding the Strategic Petroleum Reserve, in the week ending March 24, compared to the S&P Global Platts forecast for a stockpile increase of 0.3 million barrels. The American Petroleum Institute, or API, inventory data on Tuesday showed a U.S. crude inventory increase of 1.9 million barrels.

Separately, the EIA said the weekly U.S. crude oil production increased 18,000 bpd for the week ending March 24, to 9.147 million bpd. U.S. crude oil output increased 121,000 bpd to an average of 9.118 million bpd in March, compared to a February average of 8.997 million bpd. Output has fallen about 5.02% from the peak level of 9.60 million bpd in June 2015. Houston-based oilfield services company Baker Hughes Inc. said on Friday that the U.S. oil rig count rose another 10 to 662, compared to 316, when the rig count hit the low on June 6, 2016.

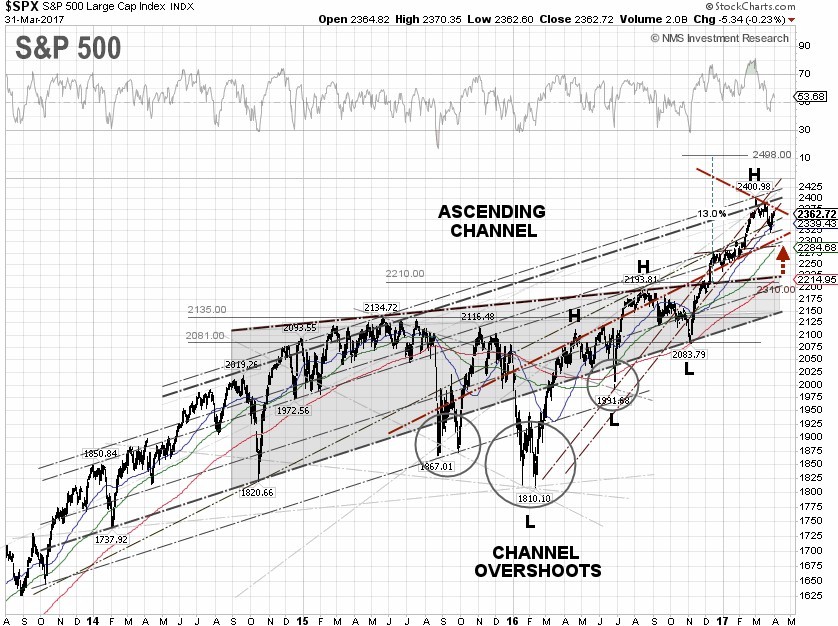

S&P 500 Summary: +5.53% YTD as of 03/31/17

Barclay Hedge Fund Index: +9.00% YTD

Outperforming Sectors: Information technology +12.16 YTD, Healthcare +7.89% YTD, Utilities +5.44% YTD, Consumer discretionary +8.09% YTD, and Consumer staples +5.64% YTD.

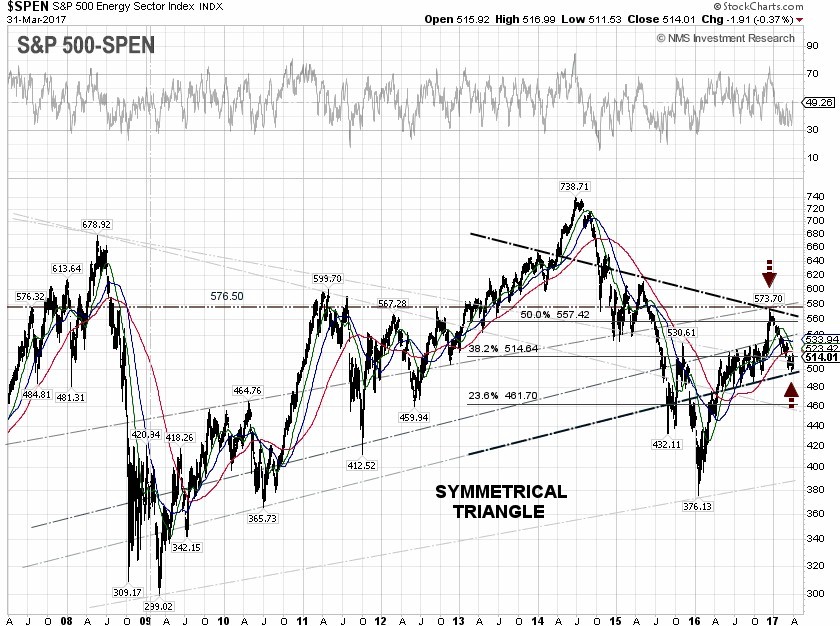

Underperforming Sectors: Materials +5.31% YTD, Industrials +4.01% YTD, Real Estate +0.78% YTD, Financials +2.08% YTD, Telecommunication services –5.06% YTD, and Energy –7.30%

YTD. |