|

The WTI crude spot price inched up 0.39% for the week, closing at $53.99 per barrel on Friday, while the Brent crude spot price gained 1.08% for the week to close at $56.33 per barrel, despite the bullish EIA weekly report on Thursday. The EIA data could be misleading though, as traders are starting to ship crude out of inventories to refineries, or exports, since the rising price of oil for near-term delivery reduces their profits, according to Reuters. To make money by holding crude, the spread between oil prices for the future months needs to be wide enough to cover the cost of leasing tank space and borrowing money to buy the fuel to fill it.

Speculative long positions in WTI crude oil futures contracts held by money managers totaled 448,846 contracts as of February 21, 2017, another record high, according to data from the U.S. Commodity Futures Trading Commission, or CFTC.

The EIA weekly U.S. oil inventory report on Thursday showed that domestic crude supplies increased by another 564,000 barrels to a record 518.68 million barrels, excluding the Strategic Petroleum Reserve, in the week ending February 17, compared to The Wall Street Journal forecast for a stockpile increase of 3.4 million barrels. The American Petroleum Institute, or API, inventory data on Wednesday showed a U.S. crude inventory decline of 884,000 barrels.

Separately, the EIA said the weekly U.S. crude oil production decreased 24,000 barrels per day, or bpd, for the week ending February 17, to 9.00 million bpd. U.S. crude oil output increased 26,000 bpd to an average of 8.968 million bpd in February, compared to a January average of 8.942 million bpd. Output has fallen about 6.59% from the peak level of 9.60 million bpd in June 2015. Houston-based oilfield services company Baker Hughes Inc. said on Friday that the U.S. oil rig count rose another 5 to 602, compared to 316, when the rig count hit the low on June 6, 2016.

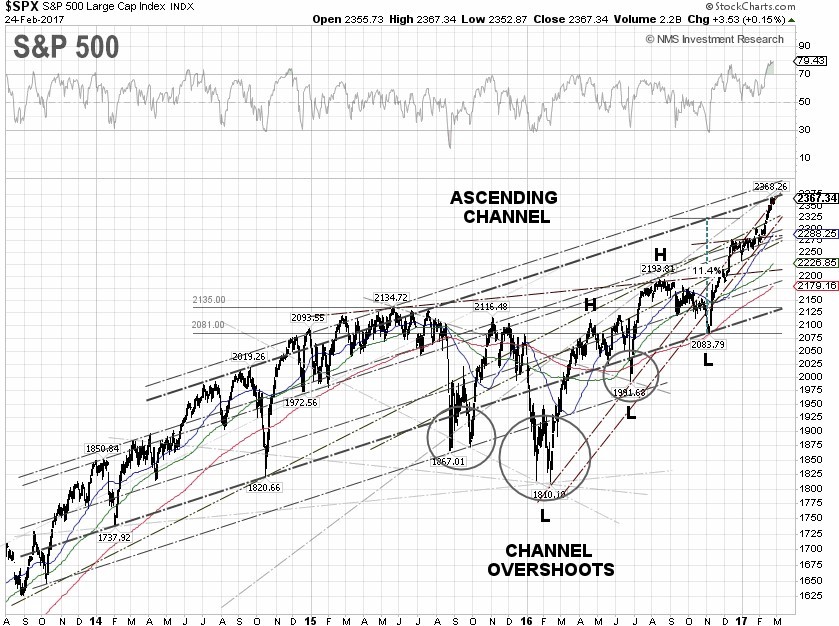

S&P 500 Summary: +5.74% YTD as of 02/24/17

Barclay Hedge Fund Index: +1.41% YTD

Outperforming Sectors: Information technology +9.94 YTD, Healthcare +8.34% YTD, Consumer staples +6.74% YTD and Consumer discretionary +6.73% YTD.

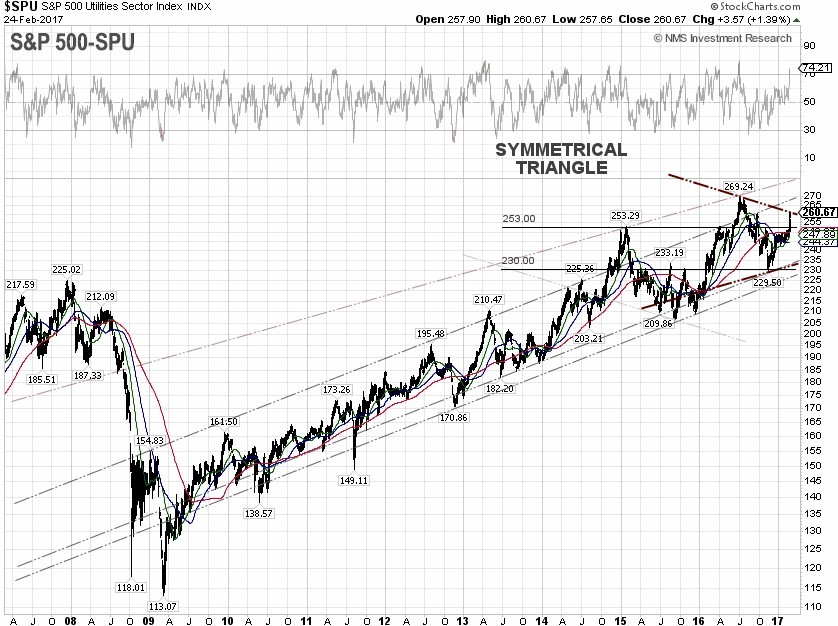

Underperforming Sectors: Utilities +5.61% YTD, Materials +5.47% YTD, Industrials +5.02% YTD, Financials +4.84% YTD, Real Estate +4.09% YTD, Telecommunication services –2.26% YTD, and Energy –6.85%

YTD. |