|

President Trump’s speech was a non-event due lack of specific details on tax policy, economic policy and infrastructure spending. The U.S. Dollar index (DXY), essentially the USD/EUR exchange rate, retested 102.16, or the 61.8% Fibonacci retracement level, on Thursday, before pulling back to close on Friday at 101.38, up 0.29% for the week, despite that New York Fed President William Dudley said on Wednesday that the case for raising U.S. interest rates has become "a lot more compelling" since the November election, given rising confidence and expectations for fiscal stimulus.

In fact, Trump’s “Phenomenal” Tax Bill could be pushed back until August, while President Trump and GOP leaders are reportedly considering punting on a major infrastructure package until 2018, as Congress wrestles with a crammed legislative calendar this year, according to The Hill.

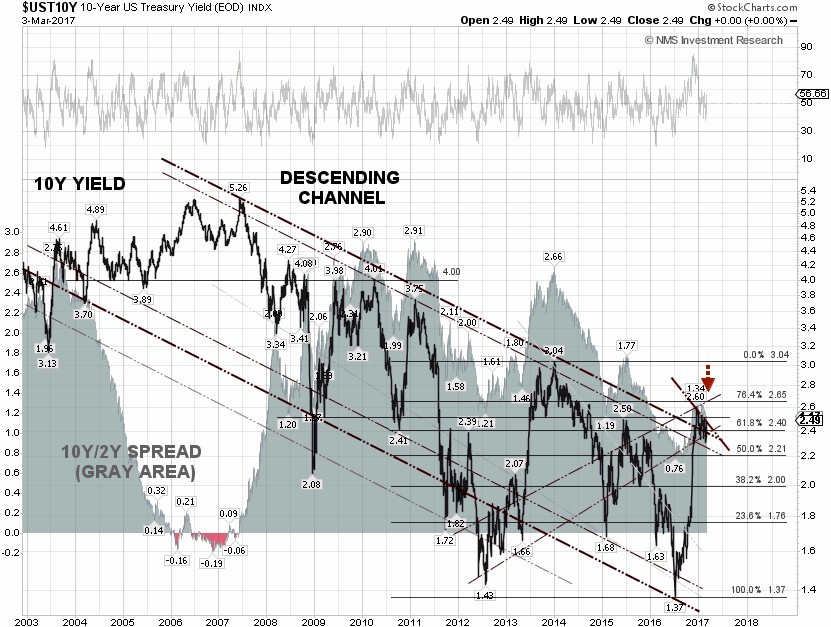

The Federal Reserve Bank of Atlanta revised its U.S. first quarter GDP 2017 on Wednesday, to 1.8% from 2.5%, citing weak real personal consumption expenditures, or PCE, after the U.S. Bureau of Economic Analysis said the core PCE index rose by 1.74% year-over-year, below expectations of 1.8%. The currency and bond markets seem to be ignoring the fact that the core PCE index, the preferred inflation indicator for the Federal Reserve, is still well below the Fed target of 2%. The median and central tendency PCE inflation projections are 1.9% and 1.7 - 2.0%, respectively for 2017, according to the Fed economic projections at the December FOMC meeting.

Late Friday, Fed Chair Janet Yellen told the audience at the Executives’ Club of Chicago that, “We currently judge that it will be appropriate to gradually increase the federal funds rate if the economic data continue to come in about as we expect.” The Fed may be pinning its hopes on the nonfarm payroll report due on March 10.

The current probability of a quarter percentage point hike, in the target of the Federal funds rate to 75 and 100 basis points at the March 14-15 FOMC meeting, is 79.7%, based on CME Group 30-Day Fed Fund futures prices. The odds that the Fed rate hike cycles will end up badly are also high. According to David Rosenberg at Gluskin Sheff, the U.S. economy landed in recession 10 out of 13 times the Fed hiked rates since WWII.

|