|

The Healthcare sector was under selling pressure for the second week in a row after President-elect Trump gave an interview to the Washington Post last weekend. Here are some excerpts from the Washington Post that moved the sector, "Trump said that lowering drug prices is central to reducing health-care costs nationally — and that he will make it a priority as he uses his bully pulpit to shape policy.

“When asked how exactly he would force drug manufacturers to comply, Trump said that part of his approach would be public pressure ‘just like on the airplane,’ a nod to his tweets about Lockheed Martin’s F-35 fighter jet, which Trump said was too costly.

“Trump waved away the suggestion that such activity could lead to market volatility on Wall Street. 'Stock drops and America goes up,' he said. 'I don’t care. I want to do it right or not at all.'”

Last week, the Healthcare sector plunged 1.91% after Mr. Trump told the media in New York during his first press conference as Presidential-elect on January 11, “we have to do is create new bidding procedures for the drug industry because they're getting away with murder.”

Berkshire Hathaway (NYSE:BRK.A) and JPMorgan Chase & Co (NYSE:JPM), 10.73% and 10.55% $SPF weighted, respectively, were down 1.06% and 2.84% for the week, despite that JPM reported better-than-expected earnings last Friday, January 13, and a sharp rise in the yield spread between the 10-year and 2-year U.S. Treasury Notes this week. Financials may be setting up for a bearish trade as the sector is now at the top of the range.

The WTI crude spot price was up 1.62% for the week, to close at $53.22 per barrel on Friday, while the Brent crude spot price dropped 0.23% for the week to close at $55.51 per barrel, despite that the EIA reported an unexpectedly large build in U.S. crude oil inventories and there was a surge in the oil rig count.

The crude prices received some support from the monthly report released by the Paris-based International Energy Agency, or IEA, on Wednesday, saying that crude oil production by OPEC members fell 320,000 barrels per day, or bpd, to 33.09 million bpd in December. Meanwhile, Saudi Arabia's energy minister Khalid Al-Falih told reporters in Davos that there's a chance of another production cut from OPEC countries this year.

The EIA weekly U.S. oil inventory report on Thursday showed that domestic crude supplies increased by 2.3 million barrels to 485.5 million barrels, excluding the Strategic Petroleum Reserve, in the week ending January 13, compared to the S&P Global Platts forecast for a stockpile decline of 900,000 barrels. The American Petroleum Institute (API) inventory data on Wednesday showed a U.S. crude inventory decrease of 5 million barrels.

Separately, the EIA said the weekly U.S. crude oil production dropped 2,000 bpd for the week ending January 13, to 8.944 million bpd. Weekly U.S. crude oil output has fallen about 6.93% from the peak level of 9.61 million bpd during the week ending June 5, 2015. Houston-based oilfield services company Baker Hughes Inc. said on Friday that the U.S. oil rig count jumped 29 to 551, compared to 316, when the rig count hit the low on June 6, 2016.

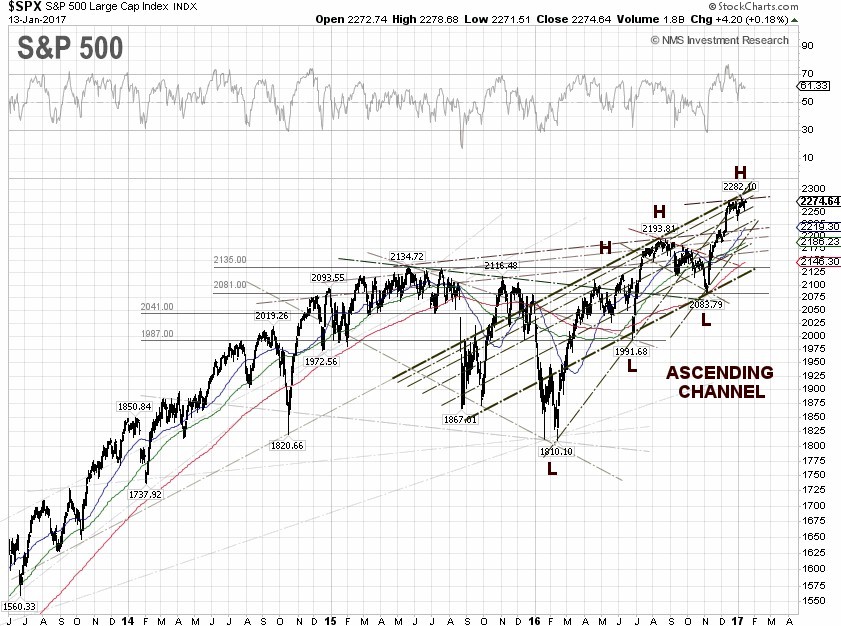

S&P 500 Summary: +1.45% YTD as of 01/20/17

Barclay Hedge Fund Index: +0.01% YTD

Outperforming Sectors: Information technology +3.47% YTD, Consumer discretionary +3.11% YTD, Materials +2.83% YTD, and Industrials +1.66% YTD.

Underperforming Sectors: Consumer staples +1.43% YTD, Healthcare +1.31% YTD, Real Estate +0.55% YTD, Utilities +0.06% YTD, Financials –0.60% YTD, Energy –1.28% YTD, and Telecommunication services –1.46% YTD. |