|

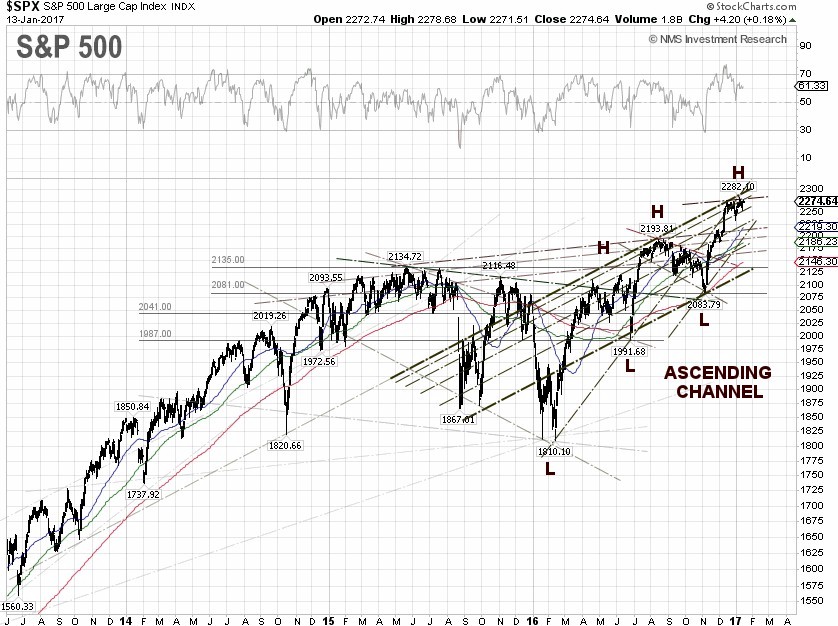

The S&P 500 managed to lose just 0.1% for the week, to close on Friday at 2,274.64, despite that the financial market was whipsawed after President-elect Trump’s first press conference on Wednesday. Wall Street was hoping for details and timelines of his economic plan, which is supposed to generate between 3.5% and 4% growth. As he put it in September before the election, “The Trump campaign's economist estimates that the plan would conservatively boost growth to 3.5 percent per year on average, well above the 2 percent currently projected by government forecasters, with the potential to reach a 4% growth rate.”, according to the Washington Post.

The S&P 500 Healthcare sector ($SPHC) plunged 1.91% after Mr. Trump said during his press conference, “we have to do is create new bidding procedures for the drug industry because they're getting away with murder.” Apparently, the market shrugged off Mr. Trump’s remark, as the S&P 500 Healthcare sector inched less than 0.1% lower for the week.

The Congressional Budget Office, or CBO, in its most recent analysis, told the Congress that the savings through negotiations alone without a stronger ability to say “no”, would be “negligible.” Tough talk negotiations with big pharma could backfire however, as it could result in limitations of drug availability and higher drug prices down the road.

Shares of defense contractor Lockheed Martin

(NYSE:LMT) plunged 2.54%, to an intraweek low on Thursday, following another of President-elect Trump's press conference remarks, “And we’re going to do some big things on the F-35 program, and perhaps the F-18 program. And we’re going to get those costs way down and we’re going to get the plane to be even better. And we’re going to have some competition and it’s going to be a beautiful thing.” Two problems with that though, the F/A-18, developed by LMT competitor Boeing

(NYSE:BA), doesn't have the stealth profile of the F-35 and no vertical-takeoff-and-landing capability.

The S&P 500 Aerospace & Defense sector, which tumbled 1.22% for the week, may recover next week after Lockheed Martin CEO Marillyn A.

Hewson, met with Mr. Trump on Friday and said that the company was “very close to a deal” to reduce the cost of the new F-35 fighter jet. According to the New York Times, Ms. Hewson also pledged to add 1,800 jobs at the Lockheed Martin Fort Worth location.

For the week, the U.S. Dollar index (DXY), essentially the USD/EUR exchange rate, closed at 101.19, down 1.0% for the week, after Donald Trump failed to deliver any specifics for his big infrastructure and tax bills at the press conference. The yield of 10-year U.S. Treasury Notes declined 0.83% this week to close on Friday at 2.4%, or the 61.8% Fibonacci retracement level, while the yield spread between the 10-year and 2-year U.S. Treasury Notes narrowed to 1.19 percentage points. The 10-year JGB yield tumbled 11% to 0.05% at the close on Friday, while the 10-year German bund yield another surged 14%, to close at 0.34%.

The WTI crude price tanked 3.0% for the week to close at $52.37 per barrel on Friday, while the Brent crude spot price dropped 2.16% to close at $55.64 per barrel, after the EIA reported an unexpectedly large build in crude oil inventories and a surge in U.S. crude oil production.

According to Reuters, the deputy leader of the UN-backed government in Libya said on Wednesday that Libya’s production rose 50,000 barrels last week to 750,000 barrels per day (bpd). The WTI crude price is now trading under the $53.96 resistance level, or 76.4% Fibonacci

retracement, as the market begins to cast doubt on the OPEC and non-OPEC production cut of 1.8 million bpd, beginning in January 2017.

The EIA weekly U.S. oil inventory report on Wednesday showed that domestic crude supplies increased by 4.1 million barrels to 483.1 million barrels, excluding the Strategic Petroleum Reserve, in the week ending January 6, compared to the S&P Global Platts forecast for a stockpile increase of 1.75 million barrels. The American Petroleum Institute (API) inventory data on Tuesday showed a U.S. crude inventory increase of 1.5 million barrels.

Separately, the EIA said the weekly U.S. crude oil production surged 180,000 bpd for the week ending January 6, to 8.946 million bpd. Weekly U.S. crude oil output has fallen about 6.91% from the peak level of 9.61 million bpd during the week ending June 5, 2015. Houston-based oilfield services company Baker Hughes Inc. said on Friday that the U.S. oil rig count dropped 7 to 522, compared to 316, when the rig count hit the low on June 6, 2016.

|