|

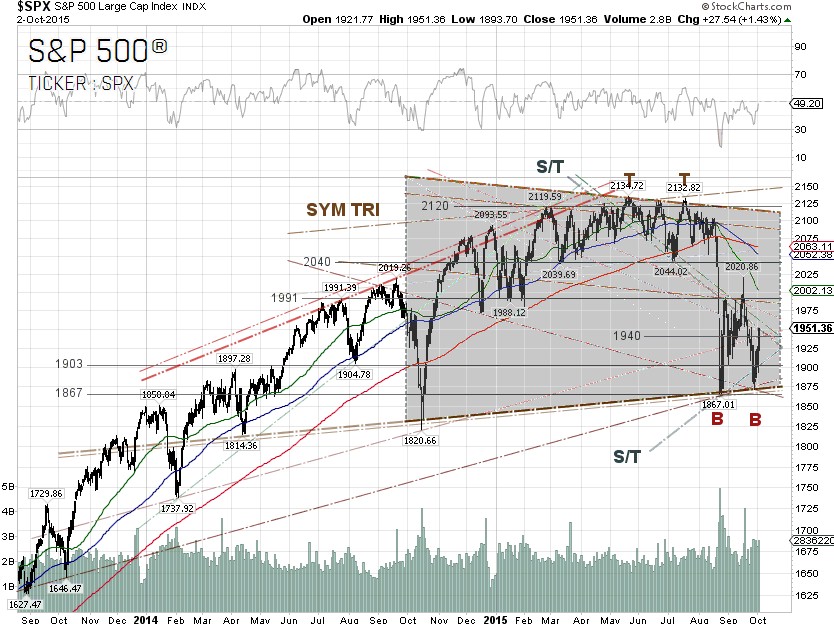

The S&P 500 took a 2.57% nosedive on Monday to close at 1,881.77 on concerns about China’s corporate profits. The China National Bureau of Statistics

(NBS) said on Monday in Beijing that the profits of industrial companies dropped 8.8% in August from a year earlier, the biggest decline since the government began releasing monthly data in October 2011, according to Bloomberg. Ironically, the U.S. markets reacted to the report more negatively than China’s markets did, as the Shanghai Composite Index closed 0.3% higher on Monday, after earlier losses.

The Conference Board, a private research group, said on Tuesday its index of consumer confidence increased to 103.0 in September from a revised 101.3 in August. The initial August reading was 101.5. Economists surveyed by The Wall Street Journal had forecast the latest index to fall to 97.0. The S&P 500 responded positively to the better-than-expected consumer confidence data but turned negative after Goldman Sachs trimmed its year-end target for the S&P 500 on Tuesday from 2,100 to 2,000, citing slower economic growth in the U.S. and China and lower-than-expected oil prices. The firm also cut its estimate for 2015 S&P 500 per-share earnings to $109, down from $114.

Buyers stepped in after the index bounced off the trendline support at 1,871.91 and took the S&P 500 higher at the close, ahead of two China manufacturing PMI reports due on Wednesday, and Friday's U.S. nonfarm payrolls report.

The S&P 500 shot up 1.91% on Wednesday, after China's official manufacturing PMI and

Caixin/Markit manufacturing PMI came in at 49.8 and 47.2, respectively, better than expectations but they are still below 50, meaning China's manufacturing sector is still in contraction. It could have been end-of-the-month/quarter window dressing when mutual funds add or trim their positions before sending out performance reports and a list of its holdings, or hedge funds scrambled for cover as the S&P has been on a downtrend since September 17.

As of September 29, there are 181,065 short positions of S&P 500 Consolidated Futures, traded on the Chicago Mercantile Exchange

(CME) by leveraged funds, an increase of 4,690 short positions from the previous week. This is compared to about 90,654 long positions, up 9,626 from the previous week, according to the Commitment of Traders (COT) data released by the Commodity Futures Trading Commission

(CFTC) each Friday.

Although hedge funds still hold a significantly large number of short positions, some hedge funds have increased their net long positions in the past two weeks by 8,082 contracts, worth about $3.9 billion, where contracts of S&P 500 futures are traded in units of $250.00 x S&P 500 index.

More bad U.S. economic news was reported on Thursday and Friday. The Institute for Supply Management (ISM) said on Thursday that its manufacturing purchasing managers index slipped to 50.2 in September from 51.1 in August, the lowest level since May 2013, noting soft global growth and the relative strength of the dollar. A reading above 50 indicates expansion in the manufacturing sector. Economists surveyed by The Wall Street Journal had expected the index to fall to 50.8.

The U.S. Commerce Department said on Friday that factory orders declined 1.7% in August after a slight gain of 0.2% in July, citing weak demand in commercial airplanes and cutbacks in investment by energy companies. Economists had expected factory orders to fall by 1.3%. Manufacturing has been under stress this year as the strong dollar has hurt export sales.

The nonfarm payrolls report released by the U.S. Labor Department on Friday was a disaster as it showed that just 142,000 jobs were added to the economy in September. The jobs report came in well below Wall Street economists' expectations of 203,000, missing expectations for four straight months. The August figures were also revised sharply downward from 174,000 to 136,000, far worse than the original forecast of 222,000. If the 136,000 jobs for August were reported a month ago, there would not have been a debate about a rate hike.

The U.S. unemployment rate remained at 5.1%, the lowest since early 2008, as more than 350,000 people left the labor force in September, pushing the labor force participation rate to a 38-year low of 62.4%, meaning 94.6 million Americans, 16 years and older, did not have a job and were not actively trying to find one.

The federal funds futures, commonly used to estimate the market’s views on the likelihood of changes in U.S. monetary policy, indicate just 5% odds for a quarter-point rate hike at the October 28 policy meeting, while the odds for a rate hike at the December 16 meeting have dropped to 30% from 41% registered on September 30, according to data from CME Group as of October 2.

Some traders had hoped that Friday's U.S. nonfarm payrolls data could help strengthen, or weaken, the case for the Federal Reserve raising interest rates before the end of the year. None of the above happened, as James Bullard, President and CEO of the Federal Reserve Bank of St. Louis, came out a couple of hours after the release of the jobs report and said that arguments that the U.S. or global economy have fundamentally changed are not compelling, or adequate to keep the Fed from raising interest rates, given the drop in unemployment and likelihood of continued growth.

Mr. Bullard practically said the Federal Reserve should not delay the rate hike. Since Mr. Bullard is currently a nonvoting member of the FOMC, he can say whatever he wants.

The yield of the U.S. 10-Year Treasury Note tumbled 8.08% for the week to close at 1.991% on Friday, while the U.S. dollar index (DXY) dropped just 0.48% for the week to close at 95.967. Technically, the dollar could weaken further if the Federal Reserve delays its rate hike or the U.S. economic outlook deteriorates.

The best performing S&P 500 sectors for the week were Energy and Materials, which climbed 2.81% and 2.71%, respectively. Both sectors trade inversely proportional to the U.S. dollar. The S&P 500 Biotechnology sub-sector rebounded 2.22% this week after investors began to sort out Hillary Clinton’s political rhetoric about her cheap drug proposals from reality.

The worst performing S&P 500 sectors for the week were Telecommunication services and Financials, which were down 1.06% and 0.61%, respectively. Top constituent of the telecommunication services sector, Verizon Communications [NYSE:VZ], tanked 3.12% for the week as the stock is stuck in the doldrums. Investors got out of the financial sector as the spread between the U.S. 2-Year and 10-Year Treasury Notes tumbled 4.08 percentage points to 1.41% for the week.

S&P 500 Summary: –5.22% YTD as of 10/02/15

Barclay Hedge Fund Index: –0.82% YTD

Outperforming Sectors: Consumer discretionary +5.13% YTD, Healthcare –0.38% YTD, Consumer staples –1.69% YTD, and Information technology –2.69% YTD.

Underperforming Sectors: Telecommunication services –8.04% YTD, Financials –8.33% (–7.77% ) YTD, Utilities –8.36% YTD, Industrials –10.36% YTD, Materials –14.92% YTD, and Energy –19.93% YTD. |