|

The

VW scandal dragged the DAX down almost 8% on Monday and Tuesday

and spilled over to the U.S. equity and emerging markets. The

whole European automobile sector practically collapsed. Deutsche

Bank trimmed the year-end target for the DAX to 10,300, from a

previous forecast of 11,300, citing a huge headwind from the

auto sector, which makes up about a 25% market cap contribution

to the German blue chips index.

As of September 22, there are 176,375 short positions of S&P

500 Consolidated Futures, traded on the Chicago Mercantile

Exchange (CME) by leveraged funds, a decrease of 642 short

positions from the previous week. This is compared to about

81,027 long positions, up 2,505 from the previous week,

according to the Commitment of Traders (COT) data released by

the Commodity Futures Trading Commission (CFTC) each Friday.

Hedge funds have increased their net long positions by 3,147

contracts from the previous week, worth about $1.6 billion,

where contracts of S&P 500 futures are traded in units of

$250.00 x S&P 500 index.

The best performing S&P 500 sectors for the second week in a

row were Utilities and Consumer staples, which climbed 1.24% and

0.74%, respectively, as investors rotated money out of high risk

sectors into defensive, safe havens that offer attractive

dividends.

The worst performing S&P 500 sectors for the week were

Healthcare and Materials, which were down 5.77% and 4.02%,

respectively, as investors were concerned about the future of

the U.S. healthcare industry under Mrs. Clinton. S&P 500

Biotechnology, a sub-sector of the Healthcare sector, plunged

9.5% for the week. The Healthcare sector is typically considered

to be defensive because the products and services are essential,

despite economic downturns. The S&P 500 Materials sector

sold off for the second week in the row, as the concern about

China's economic slowdown persists.

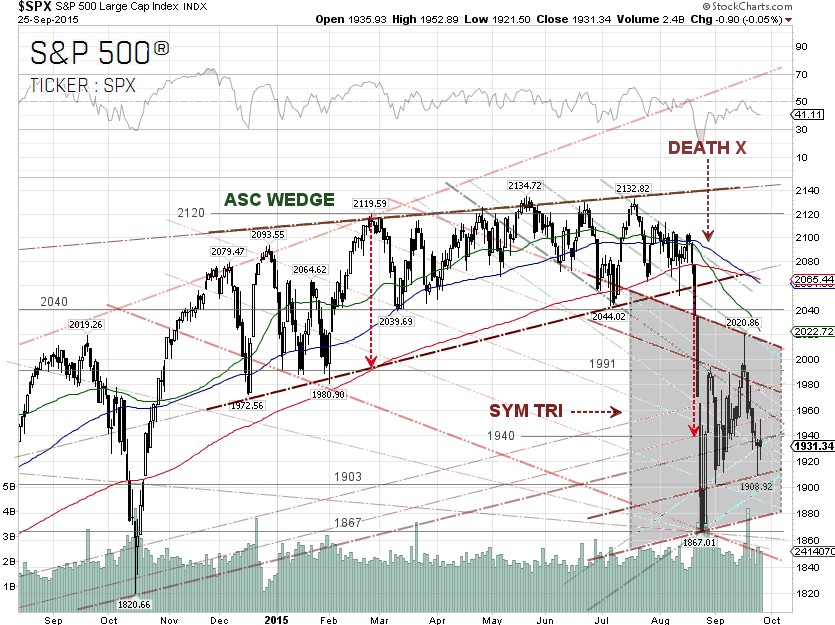

From our short-term technical viewpoint, the S&P 500 continues to move in a symmetrical triangle, in a range between the 1,991 and 1,903 levels, with downside risks increasing as the sell-side wants to see the index retest the 1,867.01 low on August 24. There are near-term supports at 1,910 and 1,880.

The headline risks for the S&P 500 are end-of-the-quarter window dressing by institutional investors, the debt ceiling crisis, the Shanghai composite index and the U.S. non-farm payrolls report due on Friday, October 2. Mr. John

Boehner, House Speaker, announced that he will resign from Congress at the end of October. There is speculation that there could be a longer-term budget agreement that also deals with raising the nation’s debt ceiling, and possibly even a major infrastructure bill, before Mr. Boehner heads back to his home state Ohio.

S&P 500 Summary: –6.2% YTD as of 09/25/15

Barclay Hedge Fund Index: +0.19% YTD

Outperforming Sectors: Consumer discretionary +3.52% YTD, Consumer staples –2.31%

YTD, Healthcare –2.4% YTD and Information technology –3.44%

YTD.

Underperforming Sectors: Telecommunication services –7.05% YTD, Financials –7.77%

YTD, Utilities –9.58% YTD, Industrials –11.41% YTD, Materials –17.18% YTD and Energy –22.12%

YTD. |