|

The S&P 500 surged 3.26% for the week to close at 2,014.89 on Friday, driven by a weak U.S. dollar and strong energy, materials and industrial sectors, as investors are convinced that the U.S. Federal Reserve will delay their first rate hike until December, or early next year. Hedge funds ran up the crude oil price 6.15% on Tuesday after a report that Russian Energy Minister Alexander Novak said Russia was ready to meet with OPEC and non-OPEC producers to discuss the market. OPEC's Secretary-General Abdullah

al-Badri also said on Tuesday that the oil exporter group should work together with producers outside OPEC to tackle the oil surplus in the global market.

The spot WTI crude oil price, traded on the Chicago Mercantile Exchange, surged 8.39% for the week to settle at $49.49 a barrel on Friday, despite the U.S. Energy Information Administration

(EIA) report on Wednesday that U.S. commercial crude-oil inventories rose to 461 million barrels, up 3.1 million barrels in the week ending October 2, about 600,000 barrels above what analysts had expected. In fact, any talks between Russia and Saudi Arabia seem to be elusive at best as Saudi Arabia demanded last week that Russia end raids in Syria, while a group of Saudi clerics are calling for jihad against the Russians in Syria.

The U.S. dollar turned lower after the Commerce Department said on Tuesday that the U.S. trade deficit widened by 15.6% month-on-month to $48.3 billion in August, as a strong dollar continues to hurt exports and demand in foreign markets remains weak. A Reuters poll of economists expected the trade deficit to come in at $47.4 billion. Analysts blamed the surge in imports in August on the Apple iPhone 6s, but net exports will weigh on overall GDP growth in the third quarter.

Minutes from the U.S. Federal Reserve’s September 16-17 policy meeting, released on Thursday, showed that Fed officials were actually concerned about low inflation and economic problems in China. There was also some disagreement between the Federal Reserve board staff, who prepare the economic projections, and Federal Reserve officials who actually vote on interest rates.

According to MarketWatch, the Fed staff’s view of the U.S. economy was much gloomier than that of the Fed officials, as the staff forecasts potential growth averaging just 1.74% over 2015-2020, while Fed officials believe that the economy can grow at 2.0%. The bad news is that the average growth rate of the U.S. economy was 3.1% over the past 50 years.

Federal Reserve Bank of Richmond President Jeffrey Lacker told Bloomberg on Thursday that the U.S. is already at full employment and the central bank may risk overheating the economy as it attempts to drive additional job gains. Some on Wall Street argue that a rate hike, when the inflation is well below the Fed’s own target, will cause the financial bull market to stumble, bond yields to climb and the economy to slip into a recession.

The federal funds futures, traded on the Chicago Mercantile Exchange

(CME) and commonly used to estimate the market’s views on the likelihood of changes in U.S. monetary policy, indicate only 8% odds for a quarter-point rate hike at the October 28 policy meeting, while the odds are 37% at the December 16 meeting, according to data from CME Group as of October 9.

As of October 6, there are 190,476 short positions of S&P 500 Consolidated Futures, traded on the CME by leveraged funds, an increase of 9,412 short positions from the previous week. This is compared to about 75,780 long positions, down 14,874 from the previous week, according to the Commitment of Traders (COT) data released by the Commodity Futures Trading Commission

(CFTC) each Friday.

Hedge funds were holding a significantly large number of short positions during the week ending October 6 as they have increased their net short positions by 24,286 contracts, worth about $12.1 billion, where contracts of S&P 500 futures are traded in units of $250.00 x S&P 500 index. We expect that the hedge funds could pull back some short positions when the CFTC reports next Friday.

The yield of the U.S. 10-Year Treasury Note surged 4.97% for the week to close at 2.09% on Friday, while the U.S. dollar index (DXY) dropped 1.13% for the week to close at 94.883. Technically, the dollar could weaken further if the Federal Reserve delays its rate hike or the U.S. economic outlook deteriorates.

The best performing S&P 500 sectors for the second week in the row were Energy and Materials, which climbed 7.77% and 6.77%, respectively. Both sectors trade inversely proportional to the U.S. dollar. The worst performing S&P 500 sectors for the week were Healthcare and Utilities, which were up just 0.25% and 1.1%, respectively. The S&P 500 Biotechnology sub-sector rebounded 0.53% this week, as traders were selling healthcare and biotech stocks and buying stocks in the S&P Oil & Gas Equipment & Services sector.

The biotech sector, particularly, was under selling pressure after the U.S. Government reached the Trans-Pacific Partnership (TPP) deal on Monday, in which it allows countries to decide between two biotech exclusivity options, either eight years of full exclusivity or five years of data exclusivity plus an additional three years of semi-exclusivity. The U.S. currently allows 12 years of exclusivity rights for biologics. Critics said the deal could cause drug prices to skyrocket, as the biopharma companies need to increase drug prices in order to recoup billions of dollars in drug development costs within 5-8 years, instead of spreading it out over 12 years.

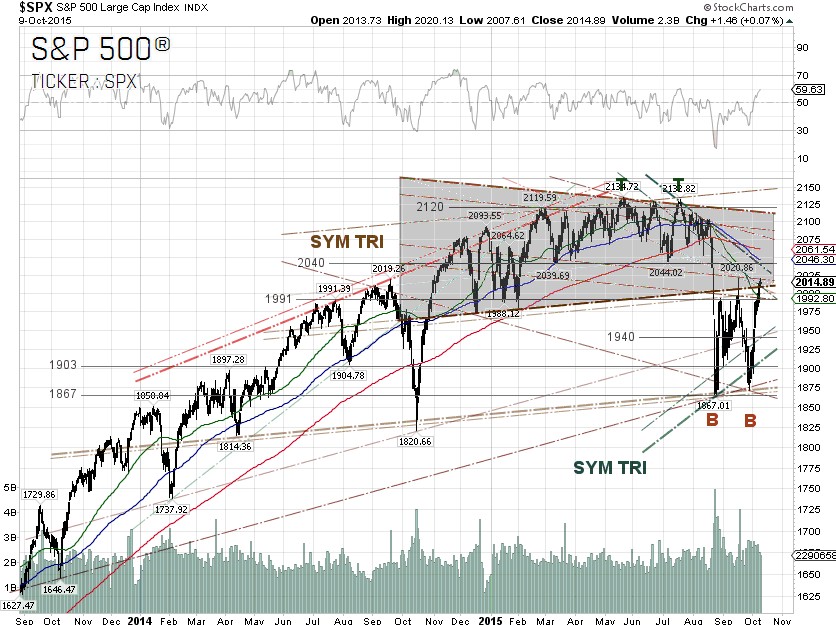

Technically, the S&P 500 broke out the key technical resistance at 1,991 and was able to close above the 50-day SMA. The index also broke back into the long-term symmetrical triangle chart pattern, with the key head resistance or overhead supply at 2,040. Investors who were trapped in the downtrend market just want to sell at the first opportunity to break even due to the overhead supply. The downside risks are a pullback in the energy sector after its big run-up in the past two weeks and a rebound of the U.S. dollar.

Traders seemed to shrug off Japan’s weak machinery orders and German trade data on Thursday. Japan's Cabinet Office said that core machinery orders, excluding those from electric power companies and those for ships, tumbled 5.7% month-on-month in August to 579.4 billion yen, missing the forecast of a 2.7% increase. Machinery orders, which are widely regarded as a leading indicator of corporate capital investment, have been on the decline for a third straight month.

The Federal Statistical Office said on Thursday that German exports dived 5.2% to 97.7 billion euros month-on-month, the steepest decline since January 2009. Imports tumbled by 3.1% to 78.2 billion euros, the biggest one-month decline since November 2012. Germany's trade surplus narrowed to 19.6 billion euros. Economists polled by Reuters had been expecting declines both in exports and imports of about 1.2% and a trade surplus of 22.5 billion euros.

S&P 500 Summary: –2.14% YTD as of 10/09/15.

Barclay Hedge Fund Index: –1.06% YTD

Outperforming Sectors: Consumer discretionary +7.69% YTD, Consumer staples 1.71% YTD, Information technology 0.71% YTD, and Healthcare –0.13% YTD

Underperforming Sectors: Industrials –4.9% YTD, Telecommunication services –5.79% YTD, Financials –6.08% YTD, Utilities –7.35% YTD, Materials –9.18% YTD. and Energy –13.71%

YTD. |