|

The S&P 500 inched up 0.9% for the week to close at 2,033.13 on Friday despite weak trade data from China and a mixed bag of U.S. economic data. The index dipped 0.68% on Tuesday after China’s General Administration of Customs said that Chinese exports fell 3.7% in September from a year earlier, in U.S. dollar terms, following a 5.5% drop in August. Chinese imports in September fell 20.4% from a year earlier, compared with a 13.8% decrease in August, while the trade surplus increased to $60.3 billion in September from $60.2 billion in August.

Economists polled by Reuters had forecast Chinese exports to decline 6.3% and imports to fall 15%. So, it was a hit-and-miss month. The National Bureau of Statistics will release China’s third-quarter gross domestic product (GDP) on Monday in Beijing. The consensus forecast is 6.8%, down from 7% in the second quarter, according to a Reuters poll of 50 economists.

On Wednesday, the U.S. Federal Reserve released its Beige Book indicating that the U.S. economy continued modest expansion at the end of the third quarter, as the strong dollar continues to hurt certain sectors of the U.S. economy including manufacturing, energy and tourism. The Federal Reserve said on Friday that industrial production slipped 0.2% in September after falling 0.1% in August. Manufacturing output, the biggest component of the industrial production index, fell by 0.1% in September, following a 0.4% decline in the prior month. It should become obvious to the Fed by now that U.S. manufacturing is in trouble.

The federal funds futures, traded on the Chicago Mercantile Exchange and commonly used to estimate the market’s views on the likelihood of changes in U.S. monetary policy, indicate only 5% odds for a quarter-point rate hike at the October 28 policy meeting, while the odds are 30% at the December 16 meeting, according to data from CME Group as of October 16.

The Commerce Department said on Wednesday that U.S. retail sales barely rose in September, edging up just 0.1% in September after being flat in the previous month. Economists polled by Reuters had forecast retail sales rising 0.2% in September. On Friday, the University of Michigan said its consumer sentiment index rose to 92.1 in early October, from a reading of 87.2 in September. Mediocre retail sales figures may not come as a surprise as consumer sentiment has been on a downtrend since the index hit a 14-year high of 98.1 in January 2015.

As

of October 13, there are 192,998 short positions of S&P 500

Consolidated Futures, traded on the CME by leveraged funds, an

increase of 2,521 short positions from the previous week. This

is compared to about 73,699 long positions, down 2,081 from the

previous week, according to the Commitment of Traders (COT) data

released by the Commodity Futures Trading Commission (CFTC) each

Friday.

Hedge

funds were holding a significantly large number of short

positions during the week ending October 13 as they have again

increased their net short positions by 4,602 contracts, worth

about $2.3 billion, where contracts of S&P 500 futures are

traded in units of $250.00 x S&P 500 index. The hedge funds

could be buying put options for protection or doubled down their

positions, as we are expecting them to pull back some short

positions when the CFTC reports on Friday.

The yield of the U.S. 10-Year Treasury Note tumbled 2.63% for

the week to close at 2.035% on Friday, while the U.S. dollar

index (DXY) dropped 0.31% for the week to close at 94.588.

Technically, the dollar could weaken further if the Federal

Reserve delays its rate hike or the U.S. economic outlook

deteriorates. The weak dollar could be due in part to the

People’s Bank of China (PBoC)’s active intervention in the

forex markets, as the PBoC has been buying yuan and selling

dollars to prevent the yuan from weakening beyond around 6.40

yuan per dollar.

Big banks, including Goldman Sachs Group Inc [NYSE:GS] and

JPMorgan Chase & Co. [NYSE:JPM], kicked off the

third-quarter earnings season with misses. According to Thomson

Reuters, third-quarter earnings are expected to decrease 4.5%

from Q3 2014.

The best performing S&P 500 sectors for the week were Utilities and Healthcare, which climbed 2.3% and 1.91%, respectively. Both sectors were the worst performing S&P 500 sectors last week. The S&P 500 Biotechnology sub-sector rebounded another 1.74% this week as the leading presidential candidates of both parties – Hillary Clinton and Donald Trump – have denounced the Trans-Pacific Partnership (TPP) deal, raising concerns that it could be held up in Congress, despite the passage of “fast-track.”

The biotech sector was under selling pressure after the U.S. Government reached the TPP deal last Monday, in which it allows countries to decide between two biotech exclusivity options, either eight years of full exclusivity or five years of data exclusivity plus an additional three years of semi-exclusivity. The U.S. currently allows 12 years of exclusivity rights for biologics. Critics said the deal could cause drug prices to skyrocket, as the biopharma companies need to increase drug prices in order to recoup billions of dollars in drug development costs within 5-8 years, instead of spreading it out over 12 years.

The worst performing S&P 500 sectors for the week were Industrials and Materials, which were down 1.21% and 0.13%, respectively. Boeing Co. [NYSE:BA], top constituent of S&P 500 Industrials, took a 4.8% nosedive on Wednesday on oversupply concerns about used wide-body planes. The poor performance of both sectors could also be attributed to U.S. industrial production, which contracted for a second month in September as lower overseas demand, as well as domestic demand, weighed on producers.

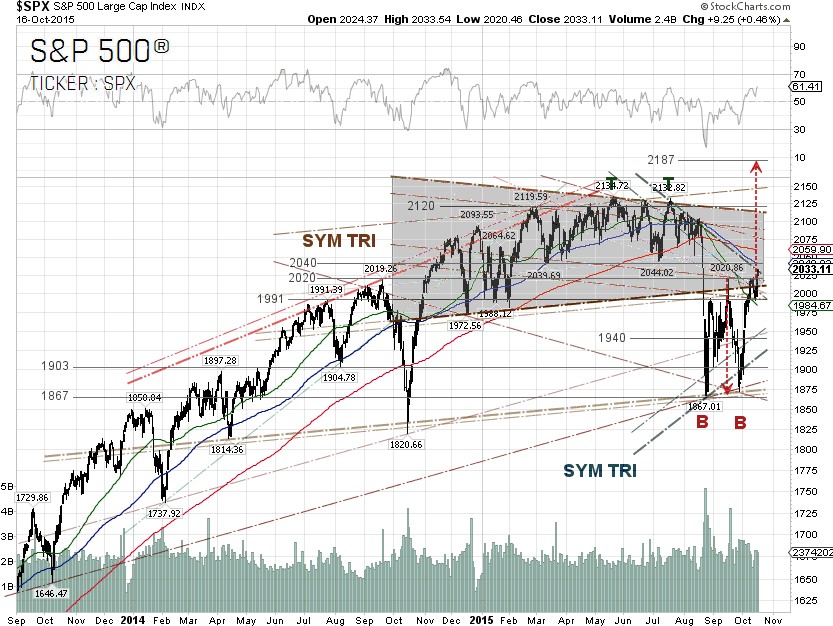

Technically, the S&P 500 broke out and closed above a key technical resistance at 2,020. The double bottom reversal is technically confirmed and the projected price for the S&P 500 is now 2,187. The key head resistance or overhead supply is 2,040, so investors who were trapped in the downtrend market might want to sell at the first opportunity to break even at that level. The downside risks are a continuing pullback in the energy sector due to a glut of supply, a rebound of the U.S. dollar, surprise negative earnings reports, and China’s GDP due on Monday.

S&P 500 Summary: –1.25% YTD as of 10/16/15

Barclay Hedge Fund Index: –1.23% YTD

Outperforming Sectors: Consumer discretionary +8.46% YTD, Consumer staples +2.12% YTD, Information technology +1.93% YTD and Healthcare +1.78% YTD.

Underperforming Sectors: Telecommunication services –4.03% YTD, Financials –4.89% YTD, Utilities –5.22% YTD, Industrials –6.04% YTD, Materials –9.29% YTD and Energy –13.07%

YTD. |