|

Ahead of the FOMC policy meeting, the Commerce Department said on Tuesday that U.S. retail sales edged down 0.1% month-over-month in February and January's sales were revised sharply downward to a 0.4% decline, from the previously reported 0.2% increase. U.S. retail sales have shown signs of trouble since it peaked in March 2015 at 1.5% month-over-month growth. Following the data release, Barclays took their consumer spending forecast down to a 2.6% annualized rate from 3.3%, and cut its U.S. GDP forecast to 1.9% from 2.4%.

U.S. consumers are feeling less optimistic as rents, medical costs and gas prices are on the rise. The preliminary reading on Friday of the Index of Consumer Sentiment by the University of Michigan hit 90 in March, down from February’s reading of 91.7. Analysts’ expectations were for 92.2, according to the Thomson Reuters consensus estimates.

As expected on Wednesday, following its two-day FOMC policy meeting, the U.S. Federal Reserve kept the key interest rate unchanged at between 0.25% and 0.5% and hinted that they may make only two rate increases by the end of the year, half the number that was forecasted at its December meeting. The Fed also trimmed its economic growth outlook for the year to 2.2%, from the previous forecast of 2.4% growth, and its forecast for inflation to 1.2% from 1.6%.

Fed Chair Janet Yellen sounded more dovish this time, compared to the December FOMC meeting press conference when she said, “Caution is appropriate,”. “Since the turn of the year, concerns about global economic prospects have led to increased market volatility and tighter financial conditions in the United States,”, added

Yellen.

The 10-year U.S. Treasury Note yield was 1.88% at the close on Friday, down 5.05% for the week. The yield spread between the 10-year and 2-year U.S. Treasury Notes closed at 1.04 percentage points on Friday, after dipping as low as 0.95 percentage point last Tuesday, a level not seen since late 2007. The U.S. dollar index

(DXY), a weighted index of the value of the U.S. dollar relative to a basket of six major currencies, closed down 1.15% at 95.12 on Friday. The DXY should bounce off this level, or else the index could be heading back to retest the 94 level.

The WTI crude oil price surged another 6.88% for the week, after headline news said that OPEC and non-OPEC producers will meet in Doha on April 17 to discuss a deal to freeze output. So far, Iran has declined to participate. Jeffrey Currie, Goldman Sachs' head of commodities research, issued a report last Tuesday saying that the recent rally in commodities is just a "mirage". Crude oil April contracts (CLJ6) will expire on Monday. Volatility due to the rollover from the April to the May contracts (CLK6) may cause price swings in either direction.

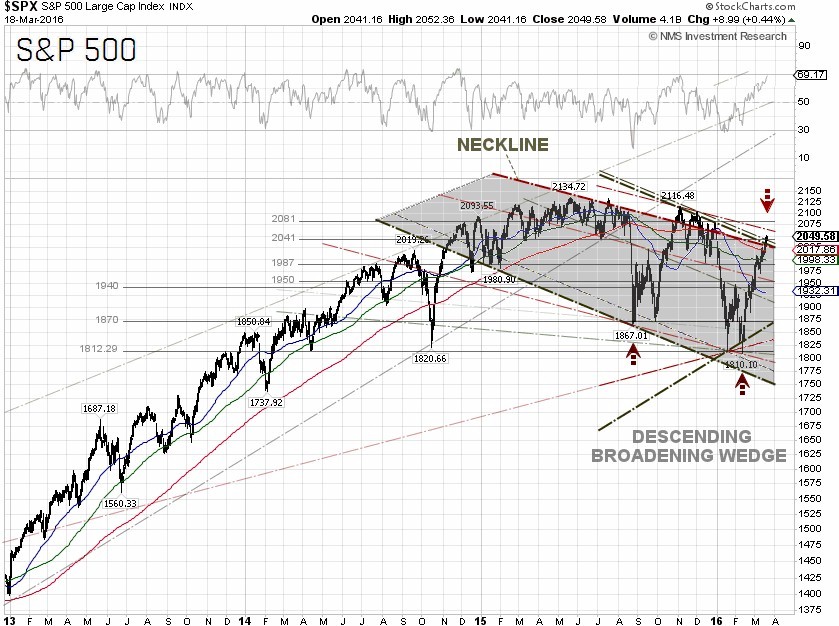

The S&P 500 closed at 2,049.58 on Friday, up 1.35% for the week, rising for the fifth week in a row. The best performing S&P 500 sectors for the week were Industrials, Energy and Materials, which were up 3.41%, 2.48% and 2.42%, respectively. Traders rotated back into the economically sensitive sectors, while still bidding up S&P 500 Utilities as a safe haven trade.

The worst performing sector for the week was Healthcare, down 2.04%. Panic sell-offs in the pharmaceutical and biotechnology sectors have been tied to the collapse of Valeant Pharmaceuticals (NYSE:VRX) share prices, down 61.25% for the week, after the company cut its earnings guidance on Tuesday and warned about a potential default on its debt due to a delayed filing. Valeant was scrutinized earlier in February by members of Congress for many things, including raising prices on existing drugs.

Earlier in the week, the Bank of Japan (BOJ) said on Tuesday that they would keep its key interest rate unchanged, but downgraded their economic outlook. That means the probability increases for more asset purchases and rate cuts deeper into negative territory at the next policy meeting in April. The BOJ is currently buying 8 to 12 trillion yen of JGBs per month, more than issued by the Ministry of Finance. In late January, the bank applied a negative 0.1% interest on excess reserves (IOER) of financial institutions placed at the BOJ, forcing the banks to extend loans to businesses or to weaker lenders. This is in an attempt to reduce borrowing costs and to drive demand for loans.

According to the Commitment of Traders (COT) data released by the Commodity Futures Trading Commission (CFTC) for the week ended March 15, there are 144,399 short positions of S&P 500 consolidated futures, traded on the Chicago Mercantile Exchange by leveraged funds, a decrease of 6,439 short positions from the previous week. This is compared to about 83,319 long positions, an increase of 1,984 from the previous week, the highest level since December 15.

The data suggests that hedge funds are increasingly bullish, but still hold a large number of short positions in their portfolios. This resulted in an increase in net long positions of S&P 500 consolidated futures by about 8,423 contracts, where contracts of S&P 500 futures are traded in units of $250.00 x S&P 500 index.

Technically, the S&P 500 is about to break out the descending broadening wedge and the double bottom (at 1,867.01 and 1,810.10) chart patterns. There is a near-term resistance at 2,081. One may want to be cautious though, as the RSI and MACD are near overbought levels.

The federal funds futures, traded on the Chicago Mercantile Exchange and commonly used to estimate the market’s views on the likelihood of changes in U.S. monetary policy, dropped to 38% odds, from 43% last week, for a rate hike at the Fed’s FOMC meeting on June 14-15, while the odds declined 3 percentage points, to 47%, for the July 26-27 meeting, according to data from the CME Group as of March 19. The market seems to think that the Fed will not do anything until its September 20-21 meeting.

S&P 500 Summary: +0.28% YTD as of 03/18/16

Barclay Hedge Fund Index: –3.27% YTD

Outperforming Sectors: Telecommunication services +13.32% YTD, Utilities +12.38% YTD, Energy +5.5% YTD, Industrials +4.53% YTD, Materials +4.23% YTD, Consumer staples +4.17% YTD and Information technology +0.36% YTD.

Underperforming Sectors: Consumer discretionary –0.04% YTD, Financials –4.63% YTD and Healthcare –7.05%

YTD. |